- By: admin

- 0 comment

Summary

Streamlined Energy and Carbon Reporting (SECR) will apply to 11,900 “large” companies and Limited Liability Partnerships from 1st April 2019. These organisations will need to collect and report on a wide range of energy data in their accounts submitted to Companies House each year.

Streamlined Energy and Carbon Reporting – Introduction

This briefing looks at the implications resulting from the issue of the Environmental Reporting Guidelines including SECR on 31st January 2019. It requires all “large” companies to include energy usage and carbon emissions data in their annual accounts filed at Companies House. It focuses on large unquoted companies and LLPs, rather than quoted companies which have slightly different requirements.

//www.gov.uk/government/publications/environmental-reporting-guidelines-including-mandatory-greenhouse-gas-emissions-reporting-guidance

Who

All large companies and Limited Liability Partnerships (LLPs) as defined under the Companies Act 2006 as meeting two of the three conditions below:

- Annual turnover of £36 million or more

- Balance sheet total assets of £18 million or more

- 250 employees or more

The government calculates that 11,900 companies will be required to report on their carbon emissions under these new regulations. Currently 1,200 quoted companies report their emissions.

It is worth noting that group reporting differs from both the CRC (Carbon Reduction Commitment) and ESOS (Energy Savings Opportunities Scheme) regulations.

Why

The UK government requires businesses to reduce their emissions in order that the country as a whole can meet the 4th carbon budget. This requires a 51% reduction of carbon emissions by 2027. To demonstrate emissions reductions successfully, businesses must first measure them and then publish them in the public domain. Stakeholders of the businesses can then see the emissions data, which they can use tis for their own decision-making. Particularly, energy saving initiatives, climate change risk and emissions within their supply chain.

When

These guidelines will apply to company financial years beginning on or after 1st April 2019.

Where

The information outlined in the Streamlined Energy and Carbon Reporting Guidance Document must be included in the Directors’ report section of the accounts submitted to Companies House.

What

Businesses must publish the following information for each financial year:

- UK energy use

- The associated Scope 1 and Scope 2 emissions

- An emissions intensity metric

- A narrative on energy efficiency action taken

- Methodologies used in the calculation of disclosures

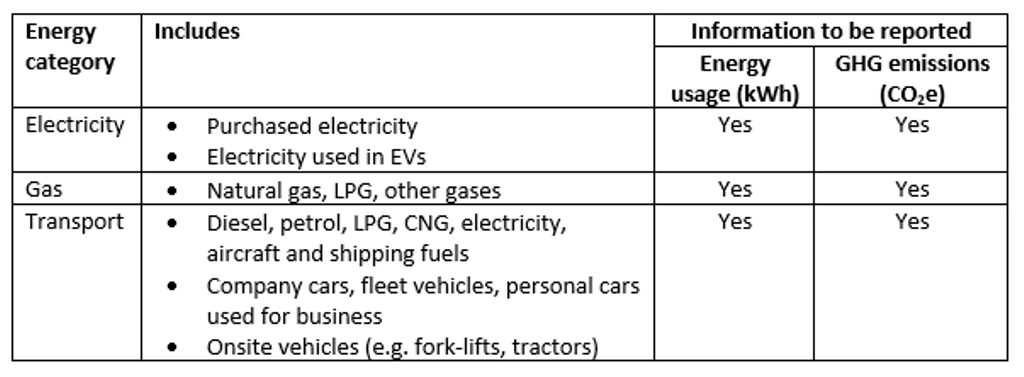

As a minimum, energy usage will include electricity, gas and transport. Transport is defined as road, rail, air and shipping. Companies will be encouraged to report their Scope 3 emissions, but this will not be mandatory. The table below shows the main areas that must be included.

The intensity metric should be relevant to the organisation’s industry, for the property sector, tonnes of CO2e per total square metres would be appropriate.

How

For many organisations, obtaining energy usage from energy billing will be the easiest way of collecting the necessary data. However, not all energy usage can be collected in this way.

Landlords can recharge energy use to a tenant, by sub-metering, as a percentage of total energy used or as part of the rent. The tenant must report this consumption, even if heat, light and power is included in the rent. It may therefore be necessary to estimate usage based on floor area using building benchmarks. This is because the legislation states “the party responsible for the consumption of energy should take the responsibility for reporting of it under this legislation”.

Transport fuels will include electricity where relevant. It also includes fuel reimbursed to employees as part of a pence per mile business mileage claim. This is the same as applies in ESOS (Energy Saving Opportunity Scheme) where it is called grey fleet mileage.

So, some organisations may face some challenges.

If you’ve any queries or would like to discuss SECR or any related areas, then please contact me.

Jean Lowes – jeanlowes@ghginsight.com or

Have a look at this page on our Website