- By: admin

- 0 comment

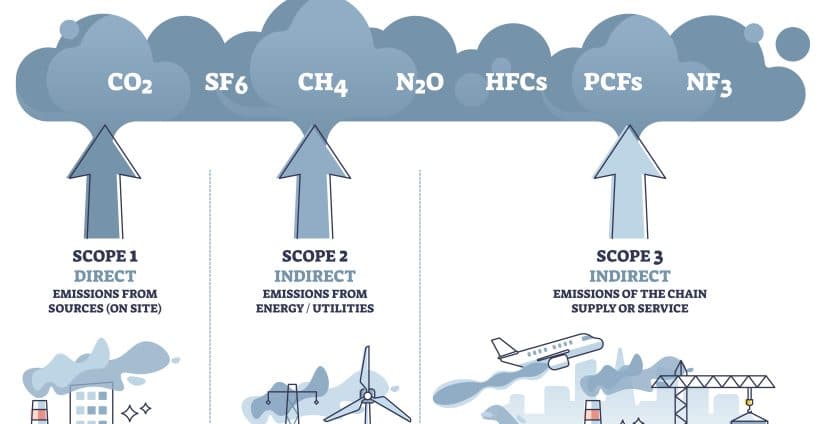

What are Scopes?

The concept of Scopes was developed by the organisation behind The Greenhouse Gas Protocol Corporate Standard. It breaks greenhouse emissions into three Scopes.

Scope 1 – Direct Emissions

These are emissions that come from sources owned or controlled by an organisation. Essentially, the greenhouse gas emissions released on an organisation’s site or from its vehicles. There are four main sources:

Stationary Combustion

This includes boilers for heating buildings, gas furnaces and gas-fired combined heat and power (CHP) plants. The most common fuels are natural gas, liquified petroleum gas (LPG), gas oil (aka red diesel) and burning oil (aka kerosene).

Mobile Combustion

All vehicles owned or leased by an organisation that burn fuels producing greenhouse gases fall into Scope 1. Typically, these will be cars, vans, trucks and motorcycles powered by petrol or diesel engines. Things are changing and plug-in hybrids (PHEVs) and Full electric vehicles (EVs) becoming more popular. The increasing use of electric vehicles could mean that some of an organisation’s fleet will fall into Scope 2 emissions.

Fugitive Emissions

Fugitive emissions are leaks of greenhouse gases, for example from refrigeration and air-conditioning units. Refrigerant gases are generally extremely potent greenhouse gases, some of which are thousands of times more damaging than carbon dioxide (CO2).

Process Emissions

These are emissions release into the atmosphere during industrial processes. These are unlikely to apply to smaller organisations.

Scope 2 – Indirect Emissions

They are the greenhouse gases released into the atmosphere from the consumption of purchased electricity, but also steam, heat and cooling. Although the CO2e emissions result from an organisation’s activities, they occur at sources it doesn’t own or control, such as a power station. As a result, they are indirect emissions.

Scope 3 – Indirect Emissions

These indirect emissions occur in the organisation’s value chain and are split into 15 categories:

| · Category 1 – Purchased goods and services | · Category 9 – Downstream transportation & distribution |

| · Category 2 – Capital goods | · Category 10 – Processing of sold products |

| · Category 3 – Fuel- and energy-related activities | · Category 11 – Use of sold products |

| · Category 4 – Upstream transportation and distribution | · Category 12 – End-of-life treatment of sold products |

| · Category 5 – Waste generated in operations | · Category 13 – Downstream leased assets |

| · Category 6 – Business travel | · Category 14 – Franchises |

| · Category 7 – Employee commuting | · Category 15 – Investments |

| · Category 8 – Upstream leased assets |

With of the exception of the transport element of Business travel, these are not required by SECR. They are relevant to organisations seeking to reach Net Zero. However, most companies will only be required to address and report on a sub-set of the categories above. The categories with green text form part of the UK Government’s PPN 06/21 requirements. Although these currently only apply to government contracts with a value of over £5 million, it is expected that commercial companies will start to request their suppliers to provide the emissions from these five categories in addition to Scope 1 and Scope 2 emissions.

What Are Scopes? Now you must measure them

If you wish help to measure your greenhouse gas emissions, we can help. Our cloud based platform GHGi Analytics is designed to simplify SECR reporting for all sizes of organisation.

Glen Winkfield

glenw@ghginsight.com

3rd April 2023

© 2023 Sustainability Vision Ltd

Glen Winkfield is Marketing Director of Sustainability Vision Ltd. Through GHGi Analytics, its cloud-based solutions, the company provides tools for organisation’s to measure, analyse and report their GHG emissions. Also available is GHGi Commuting is solution covering employee eommuting and homeworking. Sustainability Vision also offers help to organisations of all sizes, needing to develop a strategy to reach Net Zero.